TÍTULO

TÍTULO

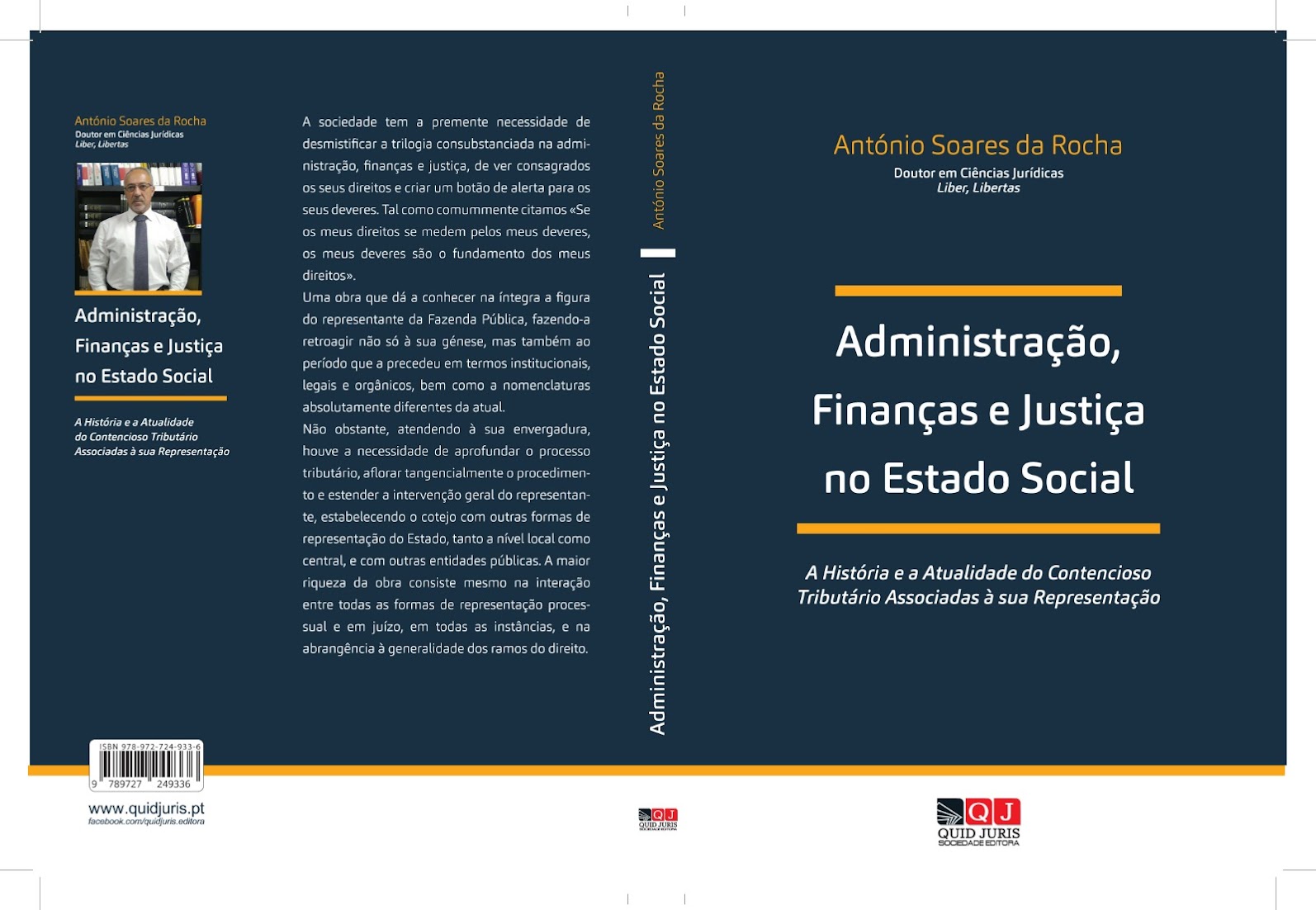

ADMINISTRAÇÃO, FINANÇAS E JUSTIÇA NO ESTADO SOCIAL

(A História e a Atualidade do Contencioso Tributário Associada à sua Representação)

Editora: Quid Juris.

Link direto: https://www.quidjuris.pt/Default.aspx?Tag=BOOK&Id=442

Dedicatória

Ao meu irmão Albino e seus filhos, Maurício e Diana.

Aos meus sobrinhos, Mateus e Matias.

Com a referência ao facto de muito humildemente com eles

ter partilhado bons princípios impregnados de esmero e inovação.

Que Deus os acompanhe no resto da caminhada que lhes é imposta.

RESUMO

Foi propósito do autor fazer o enquadramento institucional do representante da Fazenda Pública, fazendo remontar tal figura à sua génese, ou seja, à entrada em vigor do CPT (Código de Processo Tributário), sem descurar a referência prévia a diplomas que o antecederam, de modo a concretizar a cronologia daquela figura e do contencioso tributário.

E só fazendo primeiramente o seu enquadramento institucional, salta, com a génese do CPT, para o regime jurídico, fazendo-o tanto em sede de legislação tributária como a nível dos tribunais administrativos e fiscais, com a análise circunstanciada e paralela do CPTA (Código de Processo nos Tribunais Administrativos) e do ETAF (Estatuto dos Tribunais Administrativos e Fiscais), que vieram consagrar essa mesma figura nos processos onde não intervinha o MP (Ministério Público) na produção da prova testemunhal. Atendeu-se aqui, demarcadamente, à figura do representante em contraposição ao MP, que acabaria por ser extensivo aos processos de natureza criminal, onde a intervenção da Autoridade Tributária é de natureza auxiliar. Ressaltou claro, que o Estado se faz representar duplamente nos tribunais daquela natureza.

No que concerne às dívidas executivas, sendo estes processos considerados de natureza judicial, para além de se imputar inconstitucionalidade a determinados atos da AT no âmbito daqueles processos, procuramos deixar clara a posição do representante confinada ao processo judicial tributário.

Não menos importante, a menção à arbitragem tributária, processo especial de resolução de conflitos, e onde igualmente não intervém o representante. Situação que serviu para completar a necessidade de mostrar a predominância daquele, e demarcar a sua atuação, afastando situações de natureza dúbia ou onde se poderia pressupor a sua existência.

Falando do representante, não poderia ser olvidado o seu modus operandi em todos os meios processuais vigentes, sem descurar a referência aos meios impugnatórios de natureza administrativa. Em concomitância, foi dissecada a cisão da representação na AT e outras entidades, designadamente autarquias e institutos públicos.

Quanto aos tribunais, com os quais interage aquele funcionário da AT, fizemos uma leve teorização sobre a competência, o seu modo de atuação, a imparcialidade, a utilidade e princípios adjacentes.

Finalmente, uma teorização crítica, ainda que com inovações sugeridas, que refletem o pensamento isento e imparcial do autor, tendo em consideração a sua afinidade com o direito, a AT, os tribunais e o contribuinte, na concretização do projeto, na enunciação das fontes, na análise das instituições e sua especificidade, com vista à consecução do presente trabalho.

Com a progressividade da investigação, foi o autor confrontado com determinadas situações mais dúbias, desmistificando-as, mormente no que concerne à difusão do conhecimento, às fontes de direito envolvidas e a uma crítica das instituições nos seus aspetos formal e material, ex vi de umas exegese e subsunção jurídica da lei, da doutrina e da jurisprudência, em confronto com as realidades temporais.

Palavras-chave:

Representante da Fazenda Pública, representante, Fazenda Pública, representação em juízo, representação processual, estatuição do representante, competência do representante, formas de representação, função representativa, resolução de conflitos na Administração Tributária, Processo judicial tributário.

ABSTRACT

It was the author’s intent to establish the institutional setting of the representative of the Public Treasury, tracing such figure back to its origin, in other words, to the entry into force of the CPT (Tax Process Code), with no disregard of the previous reference to the legal documents which preceded it, in such a way as to materialise the chronology of such figure and tax litigation.

Only beginning with the institutional setting, may one jump on, with the origin of the CPT, to the legal framework, doing it both in the context of tax legislation and at the level of the administrative and tax court, with the contextualized and parallel analysis by the CPTA (Code of Procedure in Administrative Courts) and the ETAF (Statute of Administrative and Tax Courts) – these came to entrench that very same figure in the processes where the Public Prosecution did not intervene in the production of testimonial evidence. At this point, a clear attention was paid to the figure of the representative contrapositioned to the MP (Public Ministry), which would extend to the processes of criminal nature, where the intervention of the AT (Tax Authority) is of an auxiliary type. It was, of course, highlighted that the State is itself doubly represented on courts of such nature.

As far as the executive debts are concerned, as these processes are considered of a judicial origin, not only was unconstitutionality ascribed to certain acts of the AT within the scope of those processes, but there was also an attempt to render quite clear the position of the representative confined to the tax legal procedure.

Not of less importance is the mention to tax arbitration, a special process to resolve conflicts, where the representative also does not intervene. This situation was useful to complete the need to evidence the predominance of the latter and to demarcate its performance, moving away situations of a dubious nature or those where such existence might have been presupposed.

Regarding the representative, one must not forget the modus operandi in all current procedural means, with no disregard of the reference to the contentious means of an administrative nature. In concomitance, the fission of the representation at the AT and other entities, namely autarchies and public institutes, was dissected.

On the subject of courts, with which that element of the AT interacts, a slight theorisation was made upon its competence, its action method, impartiality, utility and adjacent principles.

Finally, a critical theorisation, even though with the suggestion of innovations, which reflect the exempt and impartial reasoning of the author, taking, into account his affinity with the law, AT, courts and the taxpayer, in the accomplishment of the project, the enunciation of the sources, the analysis of the institutions and their specificity, with the goal to attain this work.

With the progressivity of the research, the author was faced with certain more dubious situations, demystifying them, especialy as far as the diffusion of knowledge is concerned, the sources of law involved and a critique of the institutions on their formal and material aspects, ex vi of some exegesis and legal subsumption of the law, the doctrine and the jurisprudence, when confronted with the temporal reality.